Switzerland remains one of the world’s most important centers for private banking and cross-border wealth management. However, the structure of the Swiss private banking market is often discussed in broad terms, while systematic, institution-level comparisons are less common. A new ranking of the largest 69 Swiss and Liechtenstein private banks by assets under management therefore provides a useful empirical perspective on the scale, concentration and diversity of the industry.

The data show a market with two defining characteristics. First, UBS dominates the sector by a very large margin. Second, beyond UBS, Switzerland and Liechtenstein continue to host a broad and diverse private banking industry, ranging from large independent institutions to mid-sized and smaller specialized banks.

UBS as the dominant institution

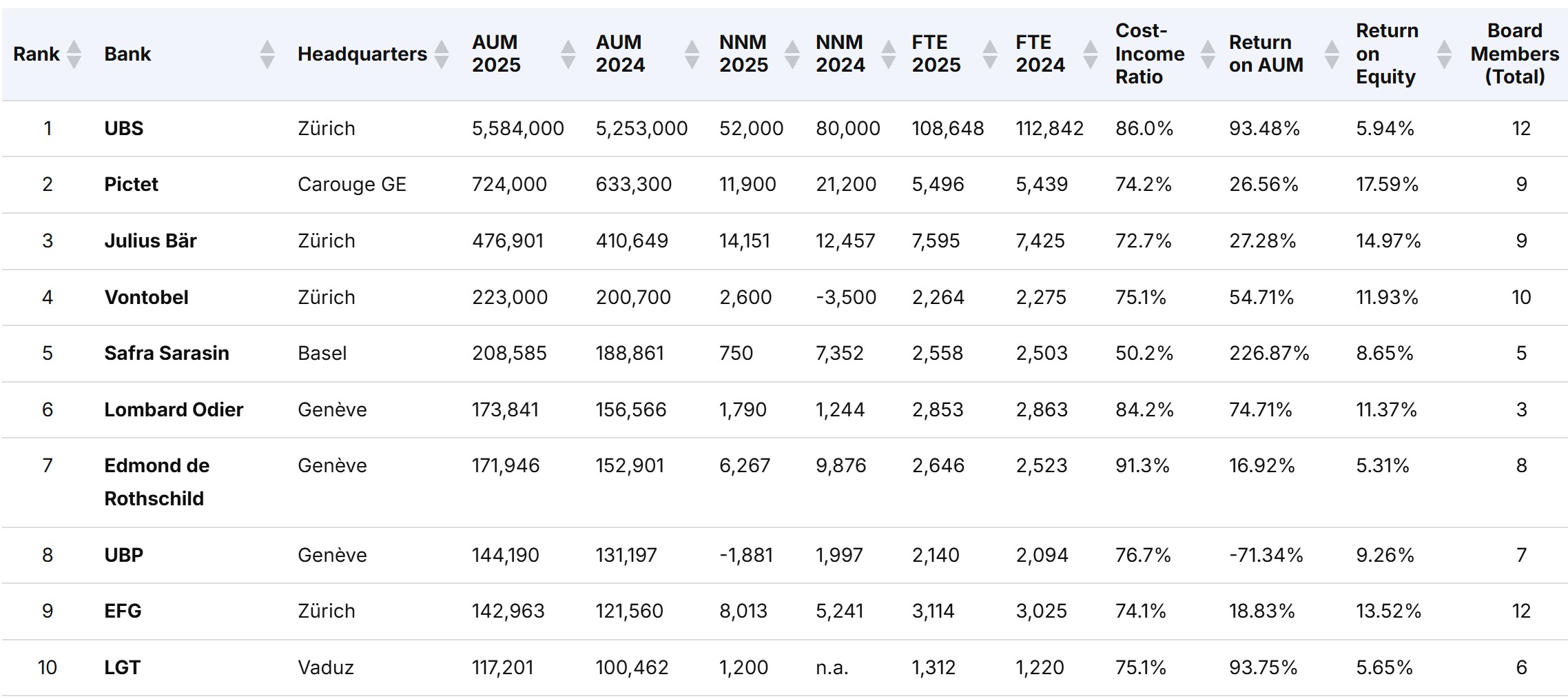

The most striking observation is the scale of UBS. With reported assets under management of CHF 5,584 billion in 2025, UBS is far larger than any other Swiss private banking institution. It does not merely lead the ranking; it represents a separate category in terms of scale.

Based on the table, UBS accounts for approximately 65% of the total assets under management covered by the ranking. This concentration has important implications for the interpretation of Switzerland’s position as a global private banking hub. A substantial part of the country’s reported private banking scale is attributable to one institution.

Without UBS, the total assets under management represented in the ranking would decline by approximately CHF 5.6 trillion. The remaining institutions would still represent around CHF 3.1 trillion in assets under management, which is substantial by international standards. Nevertheless, the scale of the Swiss private banking industry would appear materially different without UBS.

This finding highlights both strength and concentration. UBS provides Switzerland with a global wealth management institution of exceptional scale. At the same time, the data show that aggregate market size is strongly influenced by the presence of this one bank.

A broad industry beyond UBS

The dominance of UBS should not obscure the fact that the Swiss and Liechtenstein private banking sector remains broad and institutionally diverse. Beyond UBS, the ranking includes large independent private banks, partnership-based institutions, listed banks, foreign-owned banks, regional banks with private banking activities, and smaller specialized wealth management institutions.

This diversity is an important feature of the market. Institutions such as Pictet, Julius Baer, Vontobel, J. Safra Sarasin, Lombard Odier, Edmond de Rothschild, UBP, EFG and LGT illustrate the continued importance of large and mid-sized private banking institutions outside UBS. These banks differ substantially in terms of ownership model, client focus, geographic reach, governance and strategic positioning.

The ranking also shows a long tail of smaller institutions. A significant number of banks operate with assets under management below CHF 20 billion, below CHF 10 billion, and even below CHF 5 billion. This indicates that the market is not only concentrated at the top, but also highly fragmented below the largest institutions.

Such fragmentation is not unusual in private banking. The business is based not only on scale, but also on reputation, client relationships, investment capabilities, service quality and trust. Smaller institutions may face challenges related to regulatory costs, technology investments and margin pressure. However, they may also remain competitive where they have a clear client segment, specialized expertise, strong relationship management or a focused ownership structure.

Concentration and diversity as parallel features

The data therefore suggest that Swiss private banking is best described as both concentrated and diverse. It is concentrated because UBS accounts for a dominant share of the total assets under management in the ranking. It is diverse because the market below UBS consists of many institutions with different profiles and business models.

This distinction is important. AUM concentration does not necessarily mean institutional homogeneity. Even if a large share of total assets is held by one institution, the broader ecosystem may still be characterized by a wide range of competitors. This appears to be the case in Swiss private banking.

For the Swiss financial center, this structure has strategic relevance. The largest institutions contribute global scale and international visibility. Mid-sized and smaller institutions contribute diversity, specialization and client choice. The combination of both elements helps explain why Switzerland continues to be seen as a leading private banking hub.

At the same time, the structure raises questions about the future development of the sector. Rising regulatory requirements, technology investments, compliance costs and pressure on margins may affect smaller institutions disproportionately. This could lead to further consolidation, strategic partnerships or increased specialization. The ranking provides a basis for analyzing these developments over time.

Scale is only one dimension of performance

Assets under management are a central metric in private banking. They indicate scale, client reach and commercial relevance. However, they should not be interpreted as a comprehensive measure of institutional performance.

AUM says little about profitability, efficiency, risk profile, growth quality, client mix or strategic resilience (note: please refer to a published set of benchmarks for Swiss private banks for further reference). A smaller bank can be highly profitable and strategically well positioned, while a larger bank may face complexity or integration challenges. Conversely, larger institutions may benefit from economies of scale, broader investment platforms and stronger technology capabilities.

For this reason, a ranking by assets under management should ideally be read together with additional indicators. These may include net new money, cost-income ratio, return on assets under management, return on equity, number of employees and governance characteristics. Such variables make it possible to distinguish between scale, growth, operational efficiency and profitability.

This broader interpretation is particularly relevant for practitioners and researchers. AUM rankings describe market structure. Performance ratios and growth indicators provide additional insight into business quality and strategic momentum.

Relevance for research and professional analysis

Comparable data on Swiss and Liechtenstein private banks is not always easily available in consolidated form. Individual banks may publish annual reports, but disclosure levels, definitions and presentation formats differ across institutions. A structured dataset therefore helps improve comparability and supports more systematic analysis.

For researchers, such data can support empirical work on market concentration, institutional strategy, profitability, efficiency and industry structure. For students, it can be used in case studies and applied research projects. For banking executives, it provides a basis for peer comparisons and strategic benchmarking. For consultants, journalists and other professionals, it supports a more evidence-based discussion of the private banking industry.

The practical value of the dataset is increased by the availability of the table as an Excel download. This allows users to sort, filter, calculate, segment and analyze the information independently. For example, users can compare banks by size category, identify institutions below CHF 20 billion or CHF 10 billion in assets under management, analyze the distribution of AUM across the market, or combine AUM data with profitability and efficiency indicators.

Conclusion

The ranking of the largest Swiss and Liechtenstein private banks by assets under management provides a useful perspective on the structure of the private banking market. It shows the exceptional dominance of UBS, but also the continued breadth and diversity of the industry beyond UBS.

The data suggest that Switzerland’s position as a leading private banking center rests on both scale and diversity. UBS contributes a dominant share of total assets under management, while a large number of other institutions contribute institutional variety, specialized business models and competitive choice.

For a more detailed view, the full table is available on the WealthSummit page “Largest Swiss Private Banks by Assets under Management”, including assets under management, net new money, employees, profitability and efficiency indicators, and other bank-level variables. The dataset is also available as an Excel download for further analysis:

https://wealthsummit.ch/largest-swiss-private-banks-by-assets-under-management