Despite the importance of the Swiss and Liechtenstein private banking sectors, systematic benchmarking data or KPIs on Swiss and Liechtenstein private banks are not widely available in a consolidated and comparable format.

A new set of Swiss private banking benchmarks in table format provide this perspective. These tables aggregate selected key performance indicators (KPIs) for Swiss and Liechtenstein private banks and presents median, minimum, maximum and average values. The benchmarks are shown for the overall market and separately for banks above and below CHF 20 billion in assets under management.

Why private banking benchmarks matter

Benchmarking is central to strategy work in banking. It allows institutions to assess whether their performance is in line with peers, where structural differences may exist, and where management attention may be required. In private banking, this is particularly relevant because business and opeating models differ significantly.

A single performance indicator is rarely sufficient. Assets under management show scale, but not necessarily profitability. Net new money indicates commercial momentum, but does not explain cost efficiency. The cost-income ratio provides insight into operational efficiency, but not into capital strength. Return on assets under management can indicate revenue generation relative to client assets, but must be interpreted together with client mix, pricing model and service intensity.

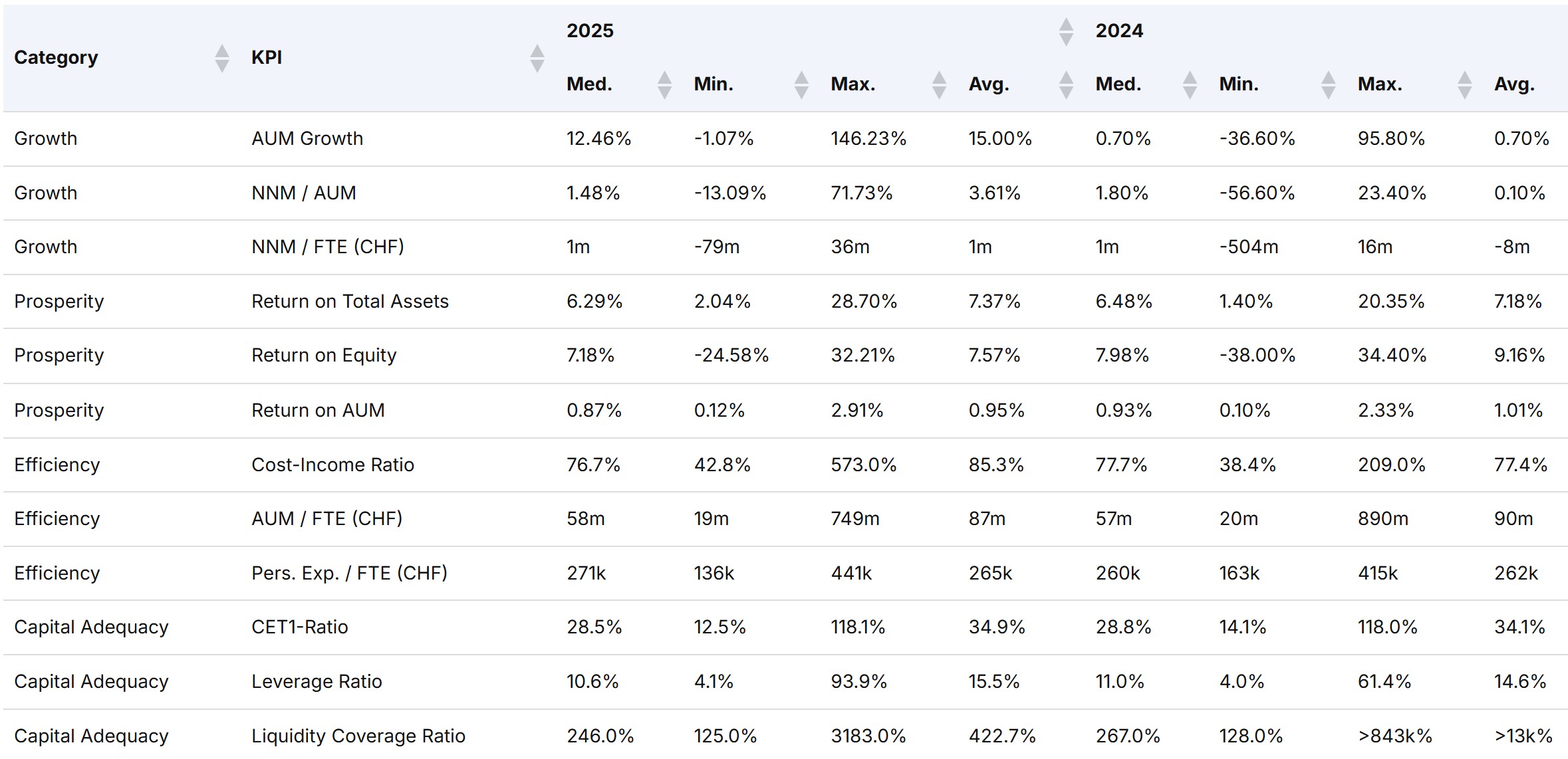

A market with significant variation

The benchmarks show substantial variation across the Swiss and Liechtenstein private banking market. This is visible across growth metrics, profitability indicators, efficiency ratios and capital adequacy measures. Such variation is not surprising. The industry includes large banks, mid-sized institutions, boutique private banks, foreign-owned banks, regional banks with wealth management units and specialized institutions with distinct client propositions.

The data also show why median values are important. Averages can be influenced by outliers, particularly in a market where institutions differ strongly in size, business model and reporting structure. Median values often provide a more robust indication of the central tendency of the market. Minimum and maximum values, by contrast, show the range of outcomes and help illustrate the heterogeneity of the sector.

Differences between larger and smaller private banks

The distinction between private banks above and below CHF 20 billion in assets under management is particularly useful. Larger private banks often benefit from scale effects. They may have broader investment platforms, larger technology budgets, more international reach and stronger institutional infrastructure. At the same time, they may also face higher complexity, larger fixed-cost bases and more demanding organizational requirements.

Smaller private banks often operate under different conditions. They may have closer client relationships, greater organizational agility and more focused business models. However, they may also face structural challenges. Regulatory compliance, technology investments, cybersecurity, risk management, reporting and platform modernization create fixed costs that can be more difficult to absorb at smaller scale.

This is where benchmark data becomes relevant. A smaller bank may not have the internal strategy department, market intelligence function or analytical resources of a large private banking group. For these institutions, external benchmarks can provide a valuable reference point.

The same applies to boards of directors. Board members need a fact-based understanding of how their institution compares with the market. Benchmarks can support discussions on strategy, risk appetite, investment needs, cost structure, capital planning and long-term positioning.

Relevance for boards and strategy consultants

For boards of directors, benchmarking provides an important governance tool. It can help move discussions from anecdotal impressions to evidence-based analysis. A board that understands how its bank compares with peers is better positioned to challenge management constructively, evaluate strategic options and assess whether the institution’s business model remains sustainable.

Strategy consultants can also use such benchmarks as an empirical basis for market studies, client diagnostics and strategic reviews. Comparable data at the level of Swiss and Liechtenstein private banks is useful not only for banks themselves, but also for advisors, researchers and other professionals working on the sector.

Scientific value of consolidated benchmark data

From a research perspective, the availability of consolidated private banking benchmarks is significant. Much of the available public information on private banks is dispersed across annual reports, regulatory disclosures, company websites and media coverage. Definitions and reporting formats may differ, and not all institutions disclose the same level of detail. A structured benchmark table helps improve comparability and allows for more systematic analysis.

Such data can support research on market structure, economies of scale, profitability, efficiency, capital strength and strategic positioning in private banking. It may also be useful for lecturing and applied research.

Access to the benchmark table

The full benchmark table is available on the WealthSummit page “Swiss Private Banking Benchmarks.” It provides aggregated indicators for Swiss and Liechtenstein private banks across growth, profitability, efficiency and capital adequacy, including separate benchmark views for banks above and below CHF 20 billion in assets under management.

The table is relevant for smaller Swiss private banks, boards of directors, strategy consultants, researchers, students and other professionals who need a structured and comparable view of private banking performance indicators. It offers a data-based reference point that is otherwise difficult to obtain in consolidated form.

The full page is available here:

https://wealthsummit.ch/swiss-private-banking-benchmarks/