As we know from Deloitte’s traditional Wealth Centre Ranking studies, Switzerland has traditionally been the world leader in cross-border wealth management, whereby the country’s significant number of External Asset Managers (EAMs) have contributed to this position. However, Swiss wealth managers have certainly faced challenges due to shifting demographics and client needs, technological advancements, regulations, or macroeconomic uncertainties.

A recent MSc thesis at ZHAW School of Management and Law by my former student Mr Fabio Metallo, who has since worked in Digital Business Technology at KPMG, has analyzed the impact of the OpenWealth Association on Switzerland’s wealth management industry. Could OpenWealth be a new source of sustainable competitive advantage?

Market Participants Facing Issues

Banks and EAMs in Switzerland are currently facing a number of operational issues around managing client assets:

- Undigitized interfaces: to manage client assets, many banks use Portfolio Management Systems (PMS), whereby data cleaning is often done manually.

- Inconsistent data quality: client data submitted by banks to EAMs may be inconsistent, whereby EAMs need to request data multiple times.

- Low transfer speed: many banks process client data at the end of trading days, whereby EAMs receive it only the next morning with previous day values.

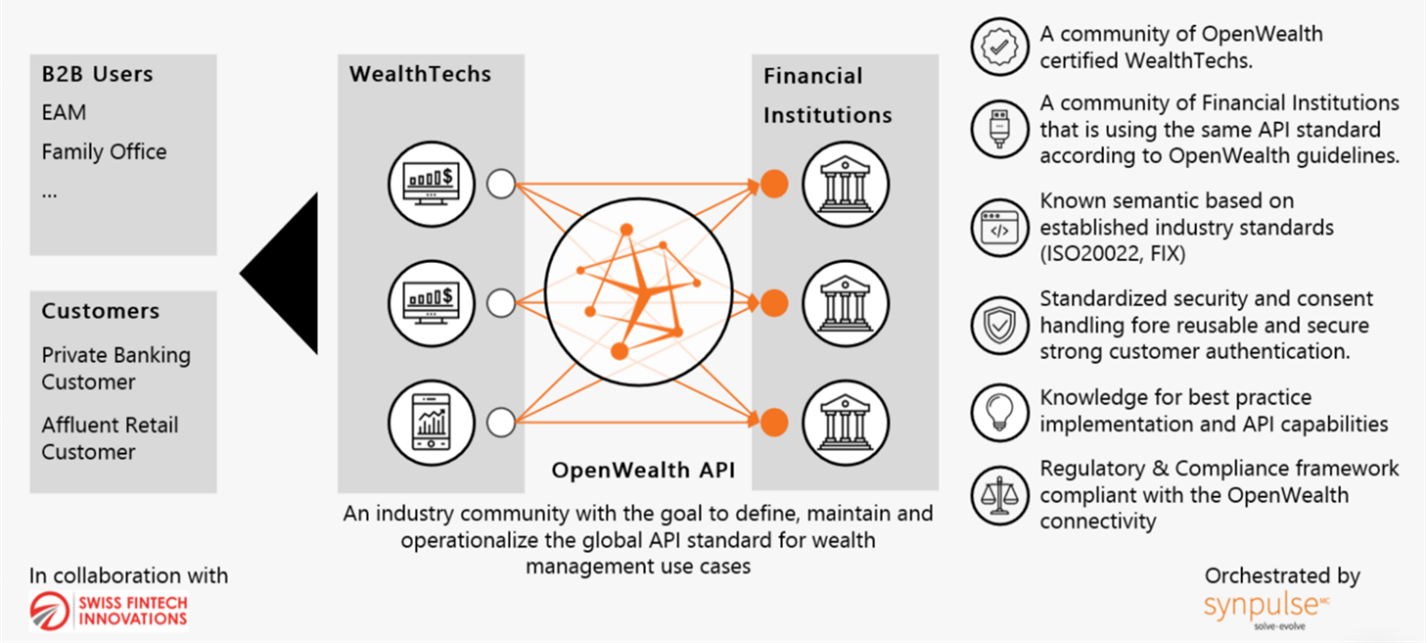

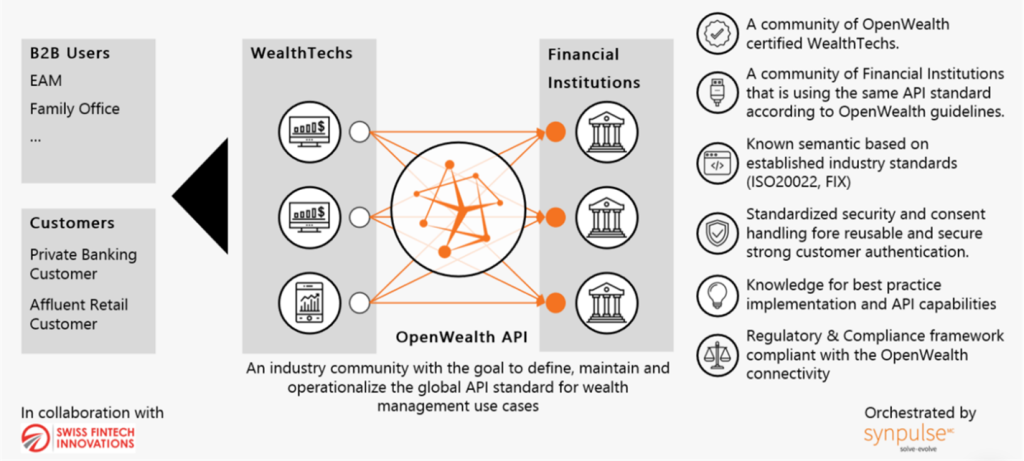

OpenWealth – Inter-Connecting Swiss Wealth Management

Switzerland’s OpenWealth Association was launched in 2021 with a vision of inter-connecting the wealth management industry (similar to open banking initiatives in European retail banking industries). It defines standards for Application Programming Interfaces (APIs), basically a set of connection points enabling banking applications to interact with other systems:

Subject to bank and client consent, OpenWealth APIs give EAMs or other firms direct access to client data stored in banks. More specifically, banks with implemented OpenWealth APIs may offer an automated exchange of documents (eliminating manual labor on both sides and enabling the exchange of real time client data). Using OpenWealth APIs is free of charge, co-creating or co-designing them requires a membership with the OpenWealth Association.

New Business Models Emerging

Wealth management clients’ ongoing demand for sustainable investments, private markets or digital assets may lead to more diverse portfolios, composed of bankable and non-bankable assets from various sources. OpenWealth may play a key role at the intersection of different industries, enabling entirely new business models: through OpenWealth APIs and Banking as a Service (BaaS) solutions, WealthTech firms may offer selected banking services without a banking license, and leverage platforms to integrate a multitude of additional services from related industries (e.g., retail banking, insurance, pension funds, even healthcare) – in line with a new generation of clients who may wish to holistically manage their wealth from a single source (without downloading multiple apps).